Smeagol domestic pharmaceutical companies race: Stone medicine starts clinical, East China medicine enters phase III …

On September 20th, East China Medicine announced that its long-acting glucagon-like peptide -1(GLP-1) receptor agonist Smegrutide injection phase III clinical trial had completed the first patient enrollment and administration. This is a multi-center, randomized, open and parallel controlled phase III clinical study. The main purpose is to demonstrate the equivalence of blood glucose control between the experimental drug Smegliclade injection and the control drug Smegliclade injection (Novotel) after 32 weeks of treatment in type 2 patients with poor blood glucose control after metformin treatment. According to the Insight database, the trial registration was announced on August 2 this year.

Test registration and historical time axis

Coincidentally, on September 18th, Unacon’s Smegliptide Injection just started its clinical trial (registration number: CTR20232854).

Registration of clinical trials of stone drugs

As a super blockbuster with annual sales of more than 10 billion dollars, smeagoutide is also competing among domestic enterprises. With the continuous advancement of clinical progress, the competition pattern is becoming more and more intense. The data show that there are as many as 12 smeagoutide similar drug projects involving domestic enterprises, and 6 of them are in phase III clinical stage.

Phase III clinical phase Smegliptide biological analogues developed by domestic enterprises.

The patent of smeagoutide in China will expire in 2026. At that time, the listing of similar drugs of smeagoutide will face huge market opportunities. In addition to the diabetes market, domestic drugs are also expected to compete with the "slimming medicine" in the 100 billion blue ocean track.

01 GLP-1: Development Potential of Multiple Indications

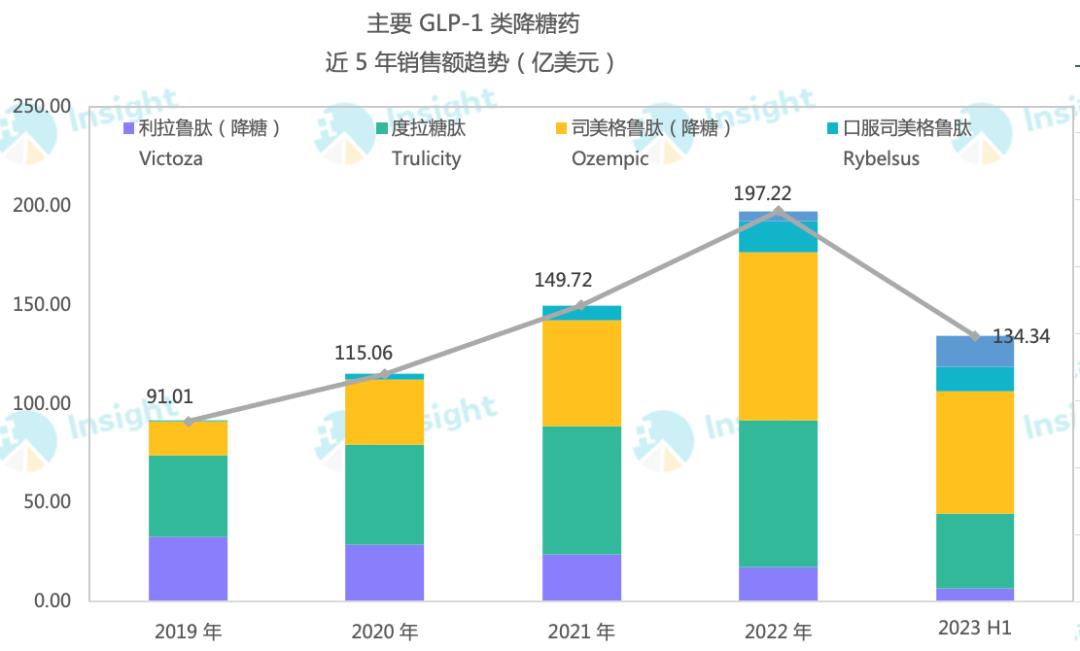

Smegliptide has 94% sequence homology with human GLP-1, which is one of the important targets for treating diabetes. As the most eye-catching GLP-1 receptor agonist in the world at present, Novo Nordisk’s smeagoutide has achieved a total sales of over 10 billion US dollars in 2022 with its good hypoglycemic and weight-loss effects, and the total sales of smeagoutide in the first half of this year has also reached 9.23 billion US dollars. According to Jost Sullivan’s prediction, the domestic market size of GLP-1 receptor agonists for hypoglycemic is expected to reach 50.1 billion yuan in 2030.

Judging from the approved indications, smeagoutide can reduce blood sugar by stimulating insulin secretion and reducing glucagon secretion, and at the same time significantly reduce the risk of major cardiovascular events (MACE) in patients with type 2 diabetes. It has been clinically approved for blood sugar control and weight loss in patients with type 2 diabetes. In addition, smegliptide is also a heavy player in the field of weight loss. The indications for obesity or overweight of novonorgestrel injection were approved by FDA in June 2021 and EMA in January 2022. Up to now, although the indications have been declared, they have not been approved in China.

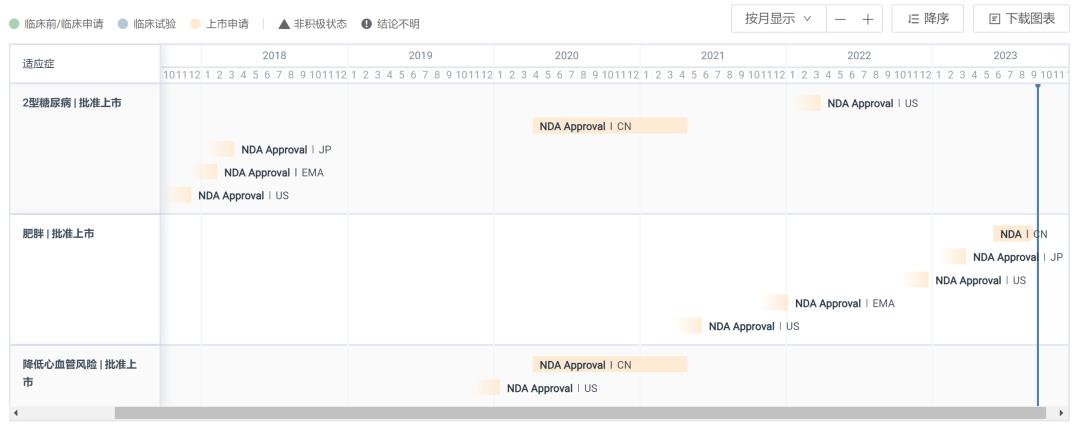

Progress in the Approval of Smegliptide in Major Regions of the World

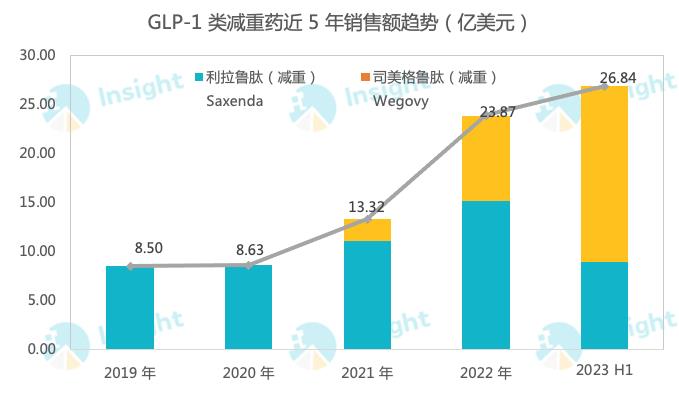

Smegliptide has great market potential in the field of weight loss, and the sales growth rate has always doubled. According to the latest semi-annual report, the sales of the drug’s weight loss indication (Wegovy) was 12.081 billion Danish kroner (about 1.781 billion US dollars), up 367% year-on-year. Moreover, due to the shortage of production capacity, Novo Nordisk also stopped advertising some of the weight-loss products of Smeagol in the United States in May this year. From another perspective, this shows that the current achievements have not reached the real strength of Smeagol’s "full firepower".

Not only that, but also in other diseases, Smegliptide has many possibilities to explore and treat. For example, in nonalcoholic steatohepatitis (NASH), it has been found that GLP-1 can reduce hepatic steatosis, hepatocyte injury and glucose output after combining with hepatic cell receptors, and reduce the inflammatory reaction and fibrosis of hepatocytes in NASH, which has the potential to treat NASH and is expected to fill the clinical vacancy of drugs for NASH diseases. In the field of Alzheimer’s disease (AD), in recent years, it has been found that GLP-1 may enhance aerobic glycolysis and reduce oxidative phosphorylation by activating PI3K/Akt pathway, and can alleviate the decline of astrocyte glycolysis induced by Aβ, which plays a role in neuroprotection and energy regulation therapy. A corresponding phase III clinical trial is being explored (registration number: NCT05891496). The step-HFpEF trial of smegliptide in treating patients with heart failure with preserved ejection fraction (hfpef) has entered the third phase. The results show that smegliptide can significantly improve the symptoms related to heart failure and exercise ability compared with placebo. In addition, some studies have found that smegliptide has cardiovascular protection, which reduces the risk of major adverse cardiovascular events (MACE). Under the background of "involution" of hypoglycemic and weight-reducing indications, other indications of smeagoutide will be explored, and in the future, the market space of smeagoutide may usher in another outbreak.

02 East China, Cinda, Hengrui … Domestic enterprises are sprinting.

From biologically similar drugs to innovative drugs, from single target to three targets, from injection to oral administration … domestic enterprises are also blocking the potential track in all directions.

1. East China Medicine: Wide layout and fast progress.

Among domestic enterprises, the layout of East China Medicine in GLP-1 field is excellent in comprehensiveness and leadership. In the field of weight loss, GLP-1 product lines covering oral dosage forms, injections and other dosage forms, including long-acting and multi-target global innovative drugs and biologically similar drugs, have been established, including the marketed liraglutide injection. The products under research include a variety of products, such as the biosimilar drug Smegliptide Injection, the global innovative oral small molecule GLP-1 receptor agonist HDM1002, the double-target agonists HDM1005 and SCO-094, and the long-acting triple-target agonist DR10624, so as to realize the all-round layout of GLP-1 with single target, double target, triple target and oral small molecules. Based on the advantages of the existing pipeline, Huadong Pharmaceutical indicated that it will continue to explore innovative projects related to GLP-1, expand the related indications such as lipid lowering and NASH, and continue to develop innovative drugs with higher bioavailability and more clinical advantages. Liraglutide, which is the first to be listed, is a medical insurance product. According to the documents exchanged by investors, the online work in more than 20 provinces in China has been completed, and it is expected that the online work in all provinces will be completed in September. The off-campus market is also the main sales channel, and offline pharmacies are expected to achieve the coverage of more than 30,000 chain retail pharmacies in the third quarter of this year. In the research product pipeline,The clinical trial of GLP-1R/GCGR/FGF21R long-acting triple-target agonist DR10624 for weight management of overweight or obese people was approved by CDE in July. In China, East China Medicine also submitted DR10624 for IND of severe hypertriglyceridemia in August this year. Abroad, in July, 2023, DR10624 completed the first subject administration in the phase I multiple incremental dose administration (MAD) clinical trial for the treatment of obesity in New Zealand. GLP-1R/GIPR double-target long-acting polypeptide agonist HDM1005 has entered the research stage of IND. At present, the project is progressing smoothly, and it is expected to submit an IND application in early 2024. HDM1002, a small molecule GLP-1 receptor agonist, has been reported in both China and the United States. In May 2023, its indication for type 2 diabetes was approved for clinical use in China, and the first trial was completed in June. The indication for overweight or obesity of HDM1002 tablets was also approved in September in China.

2. Cinda Bio’s next performance take-off point: Masidopeptide.

As early as August 2019, Cinda reached a cooperation with Lilly, and introduced GLP-1R/GCGR dual agonist Masculitide (IBI362).

Masidopeptide equity flow chart

At present, Cinda has laid out the indications for type 2 diabetes and obesity of Masculitide in China, and both of them have been promoted to phase III clinical practice. Among similar products in China, the progress is the fastest. The results of phase II clinical study showed that among the overweight or obese subjects in China, the weight of the patients decreased by 11.57% after 24 weeks of continuous administration of 6.0mg of Mastopeptide. And compared with placebo, it can bring 12.6% weight loss. In addition, among the obese patients who need surgical treatment, after 24 weeks, the average weight loss of the group using 9mg of marsden reached 15.4% and the weight loss was 14.7kg.

Results of Phase II Clinical Trial of Masculitide

The two phase III clinical codes of type 2 diabetes are DREAMS-1 and DREAMS-2 respectively, and the latter is a head-to-head clinical trial of dulaglutide; The obesity phase III clinical trial code is GLORY-1. According to the Insight database, at present, 83% of patients in DREAMS-1 have been enrolled, while the progress of GLORY-1 has been 100%.

Phase III clinical trial initiated by IBI362

Cinda said that it is expected to submit the listing application of Mastopeptide from late 2023 to early 2024. In addition to type 2 diabetes and obesity, Masculitide has also been approved for clinical use in NASH, and the corresponding research on NASH will be started soon. The listing of Mastopeptide in China will also provide Cinda with the second performance take-off point after PD-1 cindilizumab, and support Cinda to achieve the goal of 20 billion revenue in the next 4-5 years.

3, Hengrui Pharma: dual agonists, oral small molecules, compound preparations …

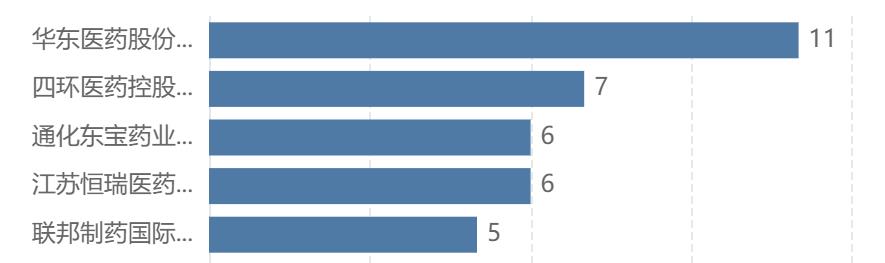

At the GLP-1 circuit, Hengrui’s layout can also be described as comprehensive. According to the layout of GLP-1/GLP-1R target enterprises, Hengrui is also among the TOP5.

Number of GLP-1R domestic enterprises’ target layout projects TOP5

Screening [target] is GLP-1/GLP-1R, excluding inactive and inactive projects for more than 3 years; Only new, improved and similar drugs are counted.

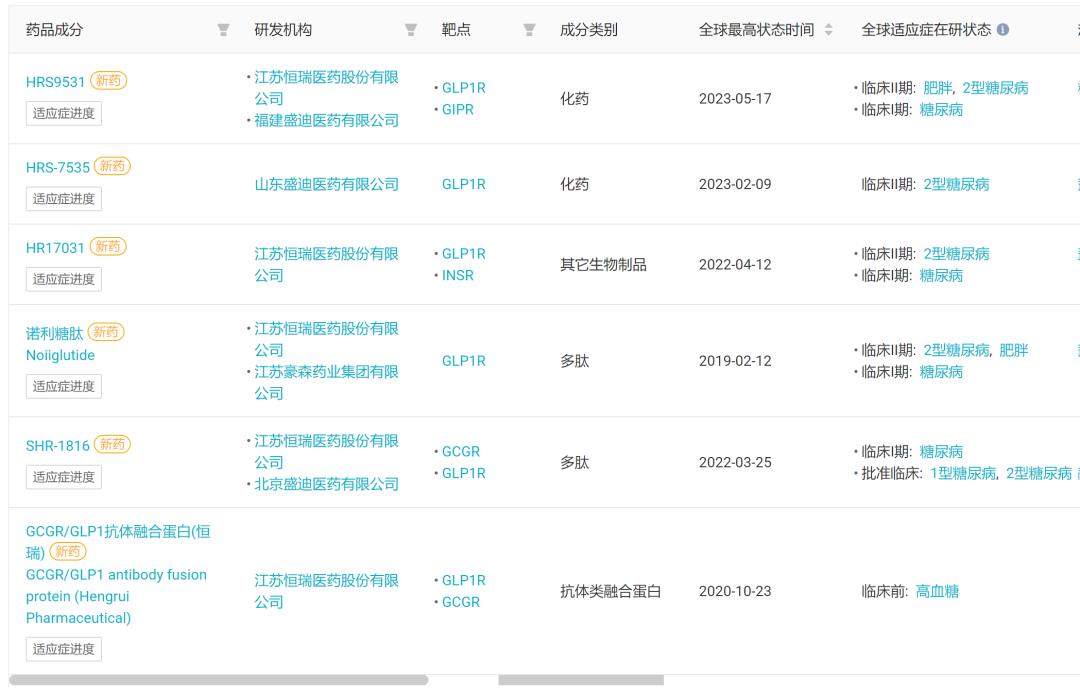

With regard to the hot GLP-1 dual-target hypoglycemic agent, Hengrui is researching GLP-1R/GIPR dual agonist HRS 9531, which has just been approved for obesity clinic in May, and has started phase II clinical research and development. In addition, Hengrui also has a GCGR antibody /GLP-1 fusion protein SHR-1816, which has also progressed to clinical stage I. In the field of small molecule oral medicine, Hengrui has HRS-7535, which has started Phase II clinical practice. In the field of compound drugs, Hengrui’s HR17031 is a GLP-1/ insulin compound drug.

Hengrui GLP-1 new drug

END

Source | Insight database